Theta Defines an Option's Time Decay

Theta, which is more commonly referred to as time decay, describes the rate at which the value of an option will erode as one trading day passes. This of course assumes that all other inputs are unchanged.

It is a calculation made from an option pricing model and forms part of a group of calculations jointly called Option Greeks, which are partial derivatives of the option price.

Why is Theta Important?

Remember that the value of an option is made up of two components; intrinsic and extrinsic value. Intrinsic value is the raw value of the option if it were exercised now. Extrinsic value is time value component that having the option to exercise represents. Because you can choose to exercise or not, having more time to do so increases the likelihood of a successful outcome. As the option approaches its expiration date, the probability of an option moving in or out of the money with respect to the underlying decreases.

Every option contract, call or put, will have zero time value at expiration and will then only be worth its' intrinsic value if exercised. So, during an option's life, it's time value is eroding each and every day. The option Theta value estimates how much of this value will erode by tomorrow.

Theta is the sensitivity of an option's price vs time to expiration.

This chart represents the daily theoretical price of a call option every day out to one year. All inputs are constant except time.

More Time vs Time Decay

Having the option to choose one thing over another is valuable and therefore the more time you have to decide adds more value to this option. For this reason, longer dated options, all other things being equal, will have more time value than shorter dated options. But this isn't the same as having a high Theta.

Theta measures the rate of decay the option will experience (all other things being equal) as ONE trading day passes. Time value is the extrinsic value until the expiration date. Take a look at this table.

| Days | Price | Theta |

|---|---|---|

| 0 | ||

| 1 | 4.18 | -4.176 |

| 2 | 5.91 | -1.73 |

| 3 | 7.23 | -1.327 |

| 4 | 8.35 | -1.119 |

| 5 | 9.34 | -0.986 |

| 10 | 13.21 | -0.678 |

| 20 | 18.68 | -0.473 |

| 30 | 22.87 | -0.384 |

| 40 | 26.41 | -0.332 |

| 50 | 29.52 | -0.297 |

| 100 | 41.74 | -0.209 |

| 200 | 59.01 | -0.147 |

| 300 | 72.24 | -0.12 |

| 365 | 79.66 | -0.109 |

This table is the theoretical output of an 1000 strike ATM call option priced out to one year. Interest rates are zero and volatility is 20% for every option. One year out, the option is valued at 79.66, which is entirely made up of extrinsic value as the underlying price and the strike price are both 1000. Here, the Theta value is only -0.11. However, as each option has time removed, its' time value decays while the Theta of the option increases.

As you can see from 5 to 1 days, the decay is clearly non-linear to the point where with one day remaining the Theta value is the same as the price of the option. Holding that at expiration all time value will be zero.

The effect of the non-liner aspect of the decay is better described in the time decay graph;

More Volatility = More Time

Theta is not only affected by time but also volatility. Options that have higher implied volatilities will also have higher Theta's than their lower volatility counterparts.

This is because volatility acts like time when it comes to an options value. The more volatile an underlying instrument, the more chances there are that the stock/future will be trading above/below the strike price of the option by the expiration date. When the underlying volatility is low, stock price movements are small and create fewer opportunities for profitable movements compared to the strikes.

Adding volatility therefore has the same effect as adding time. So, increasing the volatility increases Theta and decreasing volatility decreases Theta.

Can Option Theta be Positive?

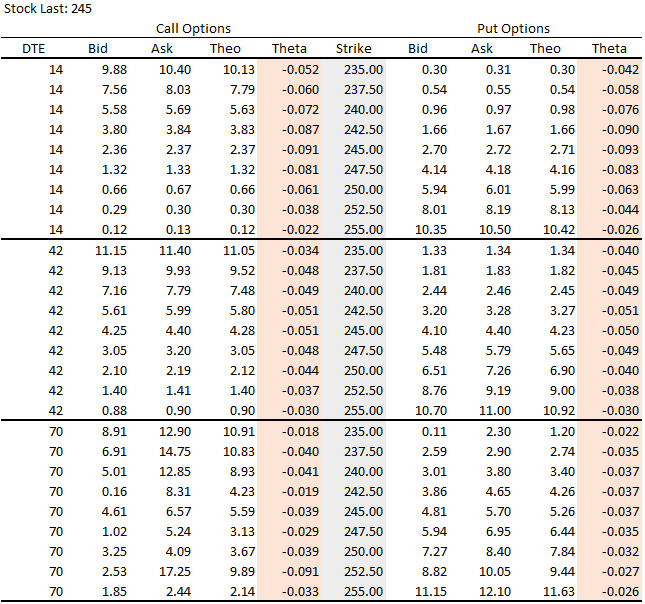

When looking at an option chain that includes theoretical prices and values the contracts are always assumed to be long. I.e the values represent prices if you were to buy the call or put.

As mentioned above, having the option to choose one thing over another loses value as time passes. Therefore the time value represented as a number must be negative. This is why Theta is always shown as a negative number for both calls and puts when pricing options. That is, it doesn't matter whether you have the option to buy or sell the stock; that option becomes worth less each day that passes. Here is what an option chain would look like;

However, if you were to sell the option your position Theta would then be positive; you would benefit from the passage of time as expiration approaches.

This is the main driver for those who profit from selling options/strategies. They sell the option, receive the premium straight away, and then benefit by keeping the premium if the option expires worthless.

Positive Theta Credit Spreads

Selling a single option will create a positive Theta position. But you can also create a positive Theta position with multiple options i.e. option spreads. If the Theta's of all the legs in the strategy combine to be positive, then your spread is said to be Theta positive.

Option traders refer to this as a strategy to "capture Theta". Typically all option credit spreads (where the net premium is received by the trader instead if paid out) will be Theta positive. For example a short condors spread is a common strategy used with retail traders as a way to generate income from a positive Theta position. This particular trade makes up the majority of the material in the popular TradingOlogy training videos. Note, I have bought this package myself so I know from experience what is inside the course.

Long & Short of it

Generally speaking, long positions will have negative Theta and short positions have positive Theta, however, not always. A good example that breaks this rule is a long calendar spread.

The net premium for this strategy will most likely be a debit i.e. you will pay money to hold this position as the longer dated option you buy will cost more than the premium you receive for selling the shorter dated option. So, this position is called a long spread. However, the Theta for this strategy will most likely be positive as the shorted dated options will have a higher rate of decay than the longer dated expiry.

Theta is the Inverse of Gamma

Remember that the Theta defines the rate of change when all other inputs remain unchanged. If, for example, the market doesn't move at all, your position will experience an approximate change according to the Theta value. Large movements in the underlying price/volatility, however, can create opportunities for an options' profitability. Movements in price and the effect the movement will have on the probability of the option is called Gamma.

Option gamma is another Greek calculation that defines the rate of change of the option delta as the underlying moves 1 full point.

Gamma has an inverse relationship to Theta. If your Theta is negative, you will want your position to experience a strong underlying price movement, hence a positive Gamma. Conversely, if your position Theta is positive you will benefit as the underlying price remains constant and lose value if the market moves hence a negative Gamma.

Black Scholes Theta Formula

Technically speaking, Theta is the first order derivative of the value of the option price and is the output of an option pricing model. There are a number of calculators that you can use to price options including my own option pricing spreadsheet. The Visual Basic formula used in my spreadsheet calculates Theta from the Black and Scholes method as;

Call Theta = -((UnderlyingPrice * Volatility * NdOne()) / (2 * Sqr(Time)) - Interest * ExercisePrice * Exp(-Interest * (Time)) * NdTwo()) / 365

Put Theta = -((UnderlyingPrice * Volatility * NdOne()) / (2 * Sqr(Time)) + Interest * ExercisePrice * Exp(-Interest * (Time)) * (1 - NdTwo())) / 365

You can see the working version of the above in the option spreadsheet.

11 Comments

Jadin December 14th, 2016 at 4:54pm

A covered call strategy is a low risk way to profit from time value decay. If the vega is high then the implied volatility will also be high and you can sell with a high option value. To make the most decay the delta (ratio of option value with respect to changes in the underlying) of a call should be close to 50 to capture the most amount of time decay.

dcclimbing January 10th, 2013 at 5:31am

Hey Omah. The graph is of the Option Price. But because the graph is dealing with an OTM option the Time value and the Option Price are the same thing because there is no intrinsic value.

I hope that makes it clearer for you.

Peter September 16th, 2011 at 6:51am

Nope, it is the price of the option.

I generated that graph by plotting the theoretical price of an OTM option and just changed the time to expiry until it was zero.

If it was an ITM option, the graph would be very similar except instead of falling at zero at zero days it would settle at the intrinsic value of the option.

Moha September 16th, 2011 at 4:18am

Excuse me, but in the graph it isn't the "Option Price" but the time value of the option !

N.B: Option Price=Time Value+ Intrinsic Value

Shahrukh October 19th, 2010 at 1:39pm

thanks

HARIOM March 12th, 2010 at 8:15pm

Good Explanation, but theta can have positive value as well and negative values.Theta is always negative for long position positive one for short position.

HARIOM March 12th, 2010 at 8:14pm

Good Explanation, but theta can have positive value as well and negative values.Theta is always positive for long position and negative one for short position.

Peter January 2nd, 2010 at 3:39am

You will have to price it using an options calculator;

optiontradingtips.com/pricing/free-spreadsheet.html

neeraj December 28th, 2009 at 6:49am

how many time value calculat for eatch day in OTM option contract

bipin September 7th, 2009 at 6:00am

nic explanation man

Add a Comment