Definition of Option Vega

The Vega of an option indicates how much, theoretically at least, the price of the option will change as the volatility of the underlying asset changes.

Vega is quoted to show the theoretical price change of the option for every 1 percentage point change in volatility. For example, if the theoretical price is 2.5 and the Vega is showing 0.25, then if the volatility moves from 20% to 21% the theoretical price will increase to 2.75.

Like Gamma, Vega is the same for both call and put options.

Vega Graphs - When is Vega Highest?

Like all other option Greeks, Vega isn't linear; it changes constantly as all other inputs to the pricing of options change. Some factors have a greater impact on the pricing of options than others. Below you'll find illustrations of the various affects these factors can have on the Vega values of options.

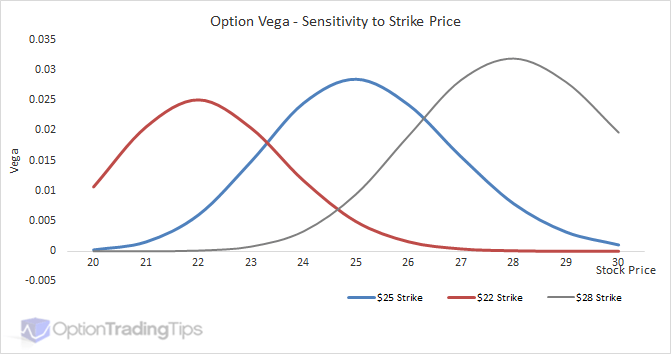

Vs Strike

ATM options are most sensitive to changes in volatility and therefore have the highest Vega values. Vega then tapers off towards OTM and ITM option strikes.

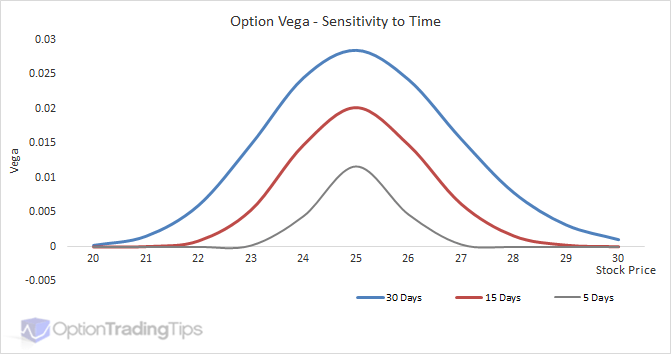

Vs Time

Volatility and time are basically the same thing when it comes to option valuation. Adding more volatility to an option is the equivalent of adding more time; that is, it increases the value of the option. The reason is that increasing either of these elements increases the likelihood of the option being in-the-money by the expiration date.

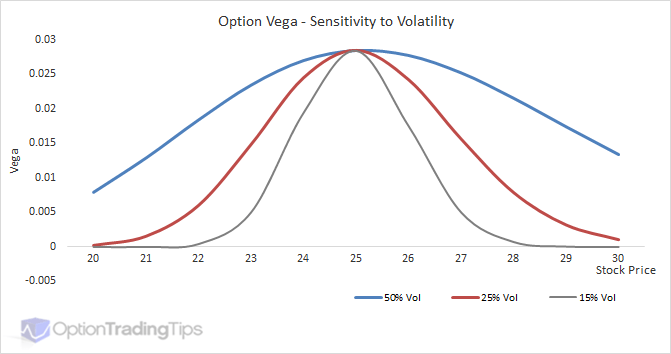

Vs Volatility

Long and Short Vega Positions

Vega has the same value for calls and puts and its' value is a positive number. That means when you buy an option, whether call or put, you have a positive Vega. This is also called being long Vega.

As Vega is effected by volatility, a long Vega position means you want the volatility to rise. When volatility rises, it will increase the value of the option by the Vega amount for every 1 % point move in the volatility. As you are long the option, the increase in the value means an increase in profit.

Conversely, short Vega positions expect volatility to fall in order to profit from a decline in option premiums.

Vega Option Chain

While theoretically the Vega is highest for ATM strikes, in practice this doesn't always happen. In the above Vega vs Strike graph, all other factors in the pricing of the option remain constant, except the strike price. I.e. The volatility input used for the pricing model is the same regardless of whether the option is ITM, ATM or OTM.

In reality, however, the implied volatility as determined by the market prices of the options are not constant; they vary across the strike range and form what's known as the Volatility Skew.

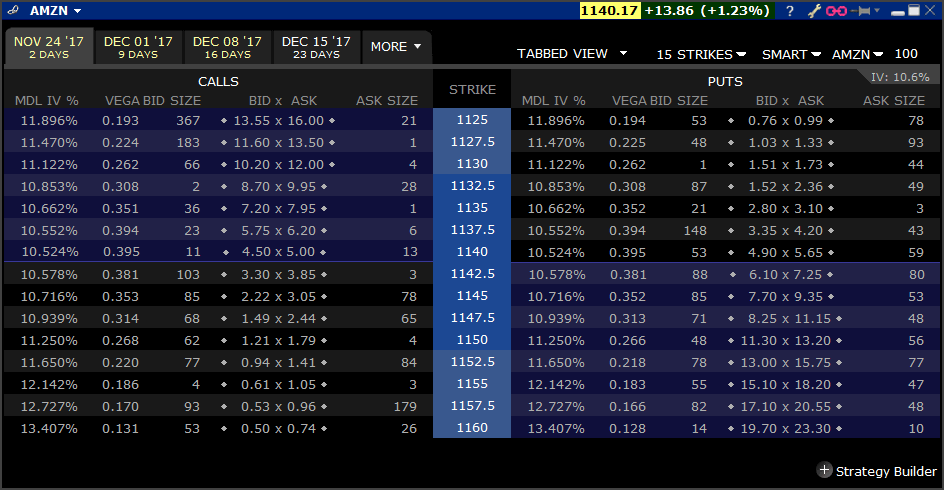

Because the volatility input is different, this can sometimes mean that the strike with the highest Vega isn't always smack on the ATM strike price. Take a look at this option chain of Amazon stock (AMZN).

I chose AMZN as it is a high priced stock, which will mean higher Vega values to observe.

These options are only 10 days out, so the forward price for this expiration will be pretty close to the stock price, which is currently 1,140.17. At this stock price the ATM strike on screen will be 1140. The Vega for this strike is 0.395. In this case, the ATM strike does indeed have the highest Vega as the strikes either side taper off and decrease as you move away from the ATM price.

However, notice the implied volatilities shown in the "MDL IV%" column? The vols show the opposite curvature to the Vega; the ATM price is the lowest while the either side of the ATM strike the implied vols increase. The changes to the volatility with this expiration aren't large enough to change the Vega values in this case, but if you do notice higher Vega values outside of the ATM strike, this is likely why.

Black Scholes Vega

Check out my spreadsheet for a working example of Vega using Black and Scholes. Otherwise, here are some code examples:

Excel VBA

Option Vega Formula

Vega = 0.01 * UnderlyingPrice * Sqr(Time) * NdOne(UnderlyingPrice, ExercisePrice, Time, Interest, Volatility, Dividend)Where:

NdOne = Exp(-(dOne(UnderlyingPrice, ExercisePrice, Time, Interest, Volatility, Dividend) ^ 2) / 2) / (Sqr(2 * 3.14159265358979)) dOne = (Log(UnderlyingPrice / ExercisePrice) + (Interest - Dividend + 0.5 * Volatility ^ 2) * Time) / (Volatility * (Sqr(Time)))

38 Comments

Vega August 1st, 2012 at 4:08pm

Hi,

I have the same question as someone ask as above. Whey is vega has a bell-curve shape. I assume the the vega should be different for in-the-money and out-of-money options?

Any insights?

Peter January 26th, 2012 at 5:58pm

The symmetrical comment below was in reference to the fact that Vega is the same value for calls and puts.

I agree that the Vega values for OTM options will have a larger percentage increase on their prices than for ITM options, however, the absolute values for Vega does indeed taper off either side of ATM to shape a bell type curve.

enter January 25th, 2012 at 7:48am

why is the vega symmetrical? wouldnt it make sense for the option price to be more sensitive to volatility when it is out of the money as opposed to in the money?

Considering, when the option is out of the money, the volatility increasing represents a higher chance of the option paying out money at the end of the day. When its in the money, the option is already most likely going to pay out money, so an increase in volatility cant (potentially) change the price as much.

Peter July 9th, 2011 at 7:06am

You mean symmetric for calls and puts? Then yes, as Vega is the same for calls and puts.

John July 8th, 2011 at 7:01am

Hi,

Thanks for this. Are the curves symmetric?

Cheers

Peter May 2nd, 2011 at 8:39pm

Vega estimates how much an option will gain or lose in value as the volatility of the underlying asset changes.

It is useful to be able to measure the amount of risk your portfolio has in relation to swings in volatility.

shrutika May 2nd, 2011 at 2:38am

What is the Vega of an option and why is it useful? Discuss the steps you would undertake to make a portfolio Vega neutral?

Pierre March 11th, 2011 at 12:18pm

So actually the value of the stock is fixed. Thanks Peter, I think I get it.

Peter March 9th, 2011 at 5:24pm

That's because Vega is the output generated from a pricing model, which is applied to an option. The option is "based" on an underlying, which can be a stock. The stock cannot have any vega because the stock "is" the underlying and doesn't have a strike price, expiration date etc.

You're probably looking at the standard deviation of the returns of a stock's movement and comparing this to the Vega of an option, which is not the same thing.

Pierre March 9th, 2011 at 5:13am

Hi,

can anyone explain me why the vega of the underlying is 0? I have read it in the Hull but don't really understand where it comes from, since when I happen to differentiate the stock price -modelled e.g. by a geometric brownian motion- with respect to sigma, the quantity does not look like 0 to me!

Thanks in advance

Add a Comment