Long Straddle

| B/S | Strike | Type | Price |

|---|---|---|---|

| Buy 1 ATM | $40 | Call | $1.14 |

| Buy 1 ATM | $40 | Put | $1.14 |

| Net Debit | $228 | ||

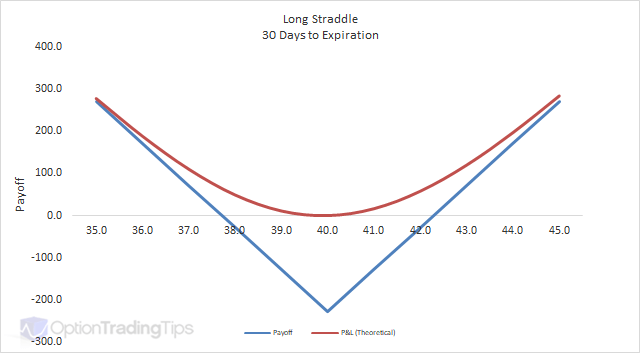

A long straddle is where you buy both a call and a put at the same strike price in the same expiration month.

The Max Loss is limited to the total premium paid for the call and put options.

The Max Gain is uncapped as the market moves in either direction.

Characteristics

When to use: When you are bullish on volatility but are unsure of market direction.

A long straddle is an excellent strategy to use when you think the market is going to move but don't know which way. A long straddle is like placing an each-way bet on price action: you make money if the market goes up or down.

But, the market must move enough in either direction to cover the cost of buying both options.

Buying straddles is best when implied volatility is low or you expect the market to make a substantial move before the expiration date - for example, before an earnings announcement.

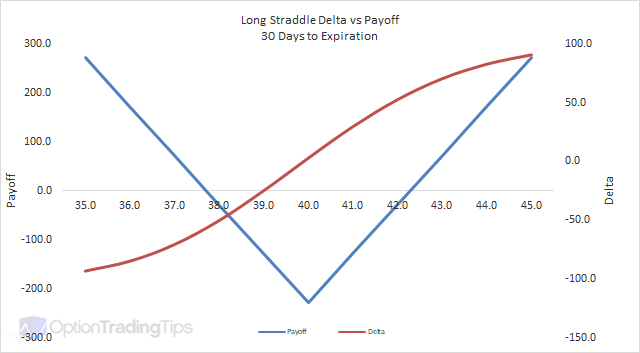

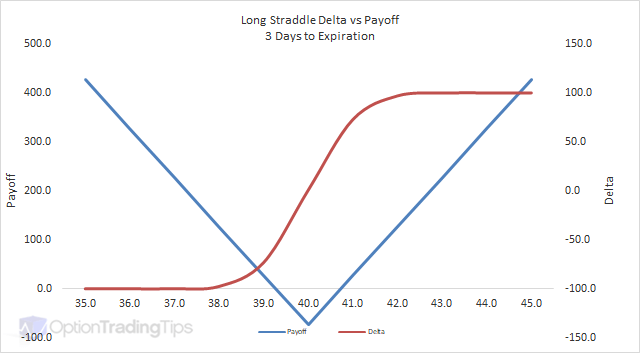

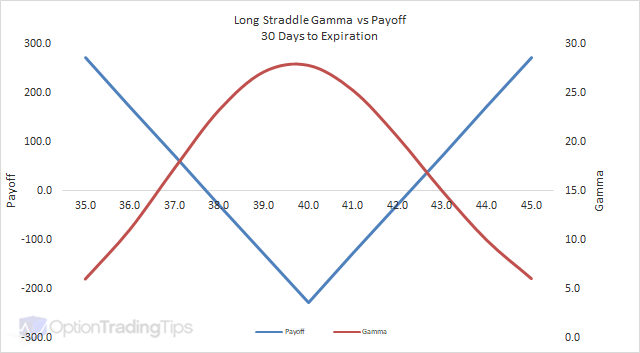

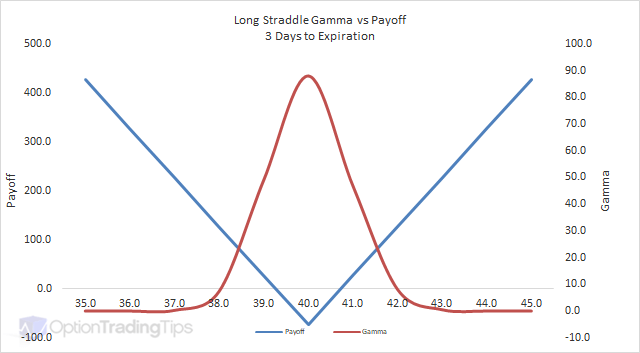

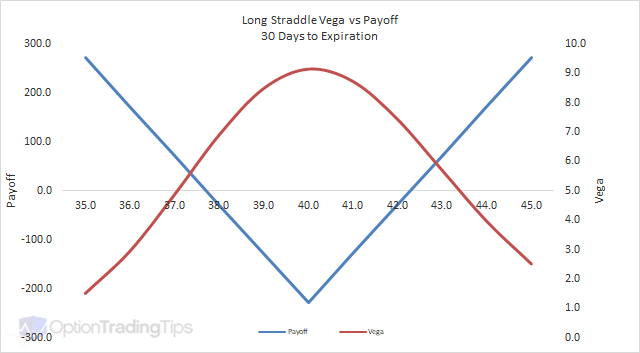

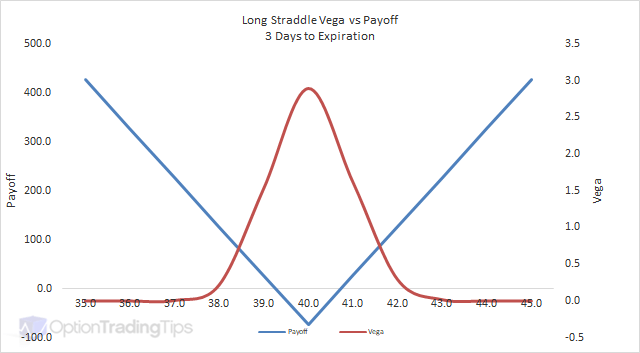

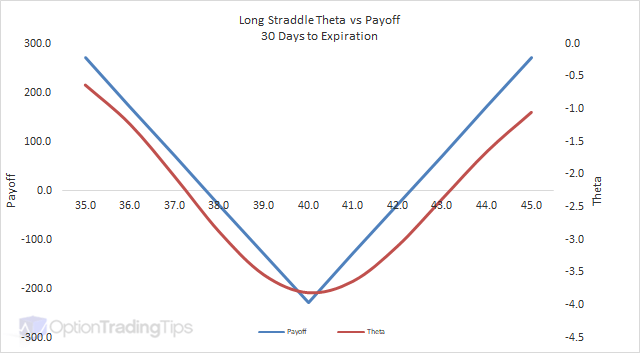

Long Straddle Greeks

Delta

Gamma

Vega

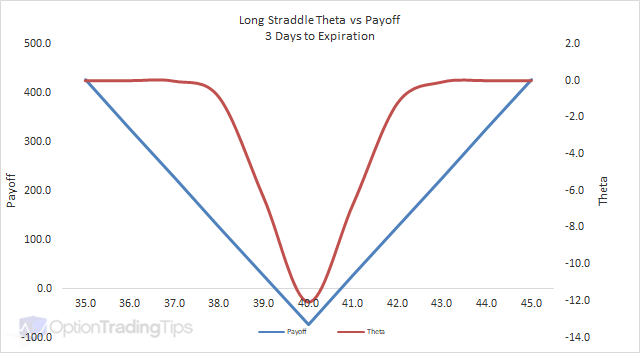

Theta

50 Comments

Jaycelle August 24th, 2014 at 4:28am

Hi Peter,

A long euro straddle, a call option on euros with an exercise price of $1.10 has a premium of $ 0.025 per unit. A put option has a premium of $0.017 per unit. The euro values at option expiration are $0.90, $1.05, $1.50, $2.00.

a) What is the net profit per unit for each possible future spot rate?

b) The break-even points of the long and short straddle?

Thanks.

Peter July 15th, 2014 at 7:24pm

Hi David,

Even though the strikes are reversed, the strategy is still called a Strangle.

Are you sure about the market prices? It would seem as if you cannot lose with those prices. What stock is it?

David July 15th, 2014 at 11:05am

Consider a stock currently trading at a price of $122. You enter into a strategy to buy a call option with an exercise price of $85 selling for $11 and a put option with an exercise price of $122 selling for $9. Both the calls and put expire in three months.

What kind of a strategy is this and why? Can someone help please

Peter July 3rd, 2013 at 5:11am

Hi Paul,

For long straddle's you just add and subtrace the total premium from the strike price. For example;

Strike: $25.00

Call Price: $5.00

Put Price: $4.50

Total premium paid is $9.50. So your breakeven points are $15.50 and $34.50.

Paul July 2nd, 2013 at 8:18am

Peter -

If I'm implementing a long straddle position, how do I model break-even?

Peter February 21st, 2013 at 2:30am

Hi Chetan,

Sure, you can use mine here ;-)

Option Trading Workbook

It uses Black and Scholes - so for European options but serves as a good framework for understand strategies and payoffs for all option markets.

Chetan February 20th, 2013 at 11:19pm

Peter, can u suggest an excel Spread sheet which can be used for Indian stocks for analyzing options and statergies., Thanks in advance.

Peter April 22nd, 2012 at 7:43pm

Hi G,

Does the OptionsXpress tool allow for paper trading? If so, that would be a great place to start. Just put aside some time to implement some of the strategies and see how they go in real.

Once you're comfortable with the ideas then you can start with small amounts of money to gain some confidence in trading options.

G April 22nd, 2012 at 12:56pm

Hello,

I'm very new to the options trading side and am using the virtual tool of OptionXpress to learn. Yet while I get the "general" gist of a call versus a put - call: betting that a stock will go up; put: betting that a stock will go down; I'm still trying to wrap my mind around the stuff beyond that like a covered call or protective put, etc. I read the definitions and can comprehend it but I'm trying to understand it and how it applies, etc.

Any recommendations?

Peter November 13th, 2011 at 6:33pm

Hi Josh,

Increasing time has the effect of higher option prices. So a straddle with a longer maturity will mean it is more expensive and hence wider breakeven points. Conversely, a shorter time frame will make the straddle cheaper and closer breakeven points.

Typically, the effect of time decay begins to decrease fastest when the options are < 30 days to expiry.

Add a Comment